Understanding LeanLaw's Billing Types: A Legal Bookkeeper's Guide to Hourly, Fixed Fee, Evergreen, and More

Jun 24, 2026If you've worked in general bookkeeping, you're used to a fairly straightforward revenue model: a service is performed, an invoice is sent, and payment is received. Law firms, however, operate with a surprisingly wide variety of billing arrangements — and each one has its own accounting implications, trust account considerations, and revenue recognition rules.

As a legal bookkeeper, understanding how each billing type works — and how LeanLaw handles them — is essential to keeping your firm's books accurate, compliant, and audit-ready. Get this right, and you'll be an invaluable asset to the attorneys you support. Get it wrong, and you could be looking at trust account discrepancies, misrecognized revenue, and some very uncomfortable conversations with the state bar.

This guide breaks down the most common billing types you'll encounter in LeanLaw, what makes each one unique, and exactly what you need to know to manage them with confidence.

Why Billing Types Matter in Legal Bookkeeping

Before we walk through each billing type, it's worth understanding why this matters so much in a legal context specifically.

In most businesses, revenue recognition is simple: money in equals revenue earned. In law firms, it's more nuanced. A client might pay $10,000 upfront that the attorney hasn't earned yet. Or an attorney might complete an entire case before collecting a single dollar. Some arrangements bill for time as it's worked; others bill a flat amount regardless of the number of hours spent.

Each of these scenarios requires different handling in LeanLaw — and different accounting treatment in QuickBooks. Knowing which billing type a matter uses before you start touching the books will save you from costly corrections down the road.

Hourly Billing

What it is: The attorney tracks time spent on a matter and bills the client at a set hourly rate. Different timekeepers (partners, associates, paralegals) may have different rates on the same matter.

How it works in LeanLaw: Timekeepers log time entries against a specific matter throughout the month. At billing time, those entries are compiled into a draft invoice, reviewed, approved, and sent to the client. LeanLaw allows you to set individual billing rates by timekeeper and by matter, giving the firm flexibility to customize rates for different clients or case types

What bookkeepers need to know:

-

Revenue is recognized when the invoice is generated and sent, not when the time is entered

-

Keep a close eye on the unbilled time report — time entries sitting in draft status are not yet revenue

-

Write-offs and discounts applied at invoice approval reduce the billable amount and should be tracked carefully

-

If the client has a retainer on deposit in trust, LeanLaw can apply trust funds to pay the invoice — this triggers a transfer from the trust account to the operating account, which must be recorded correctly in QuickBooks

Common legal bookkeeping mistake: Recording trust deposits as income when they're received. Trust funds are a liability, not revenue — they don't become income until they're applied to an earned invoice.

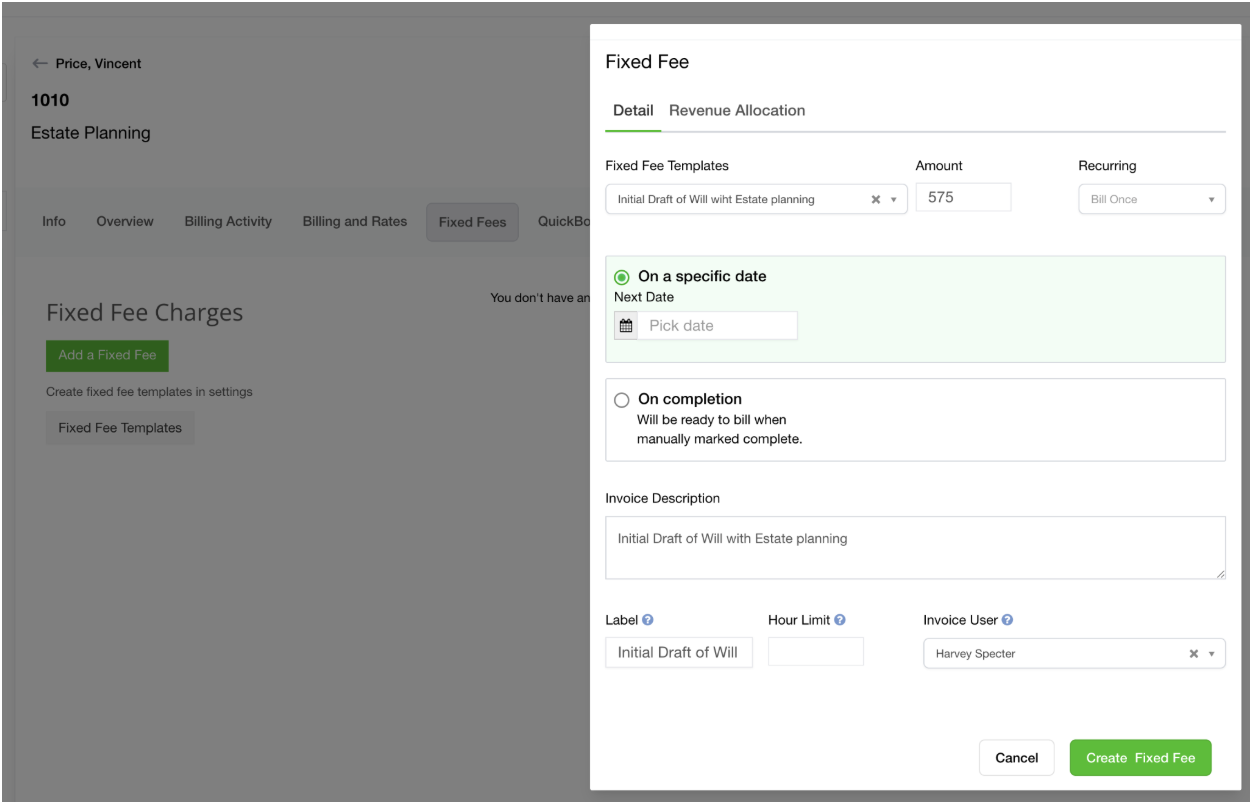

Fixed Fee (Flat Fee) Billing

What it is: The attorney and client agree on a set fee for a defined scope of work, regardless of how many hours it takes. Common in practice areas like estate planning, business formations, simple divorces, and criminal defense.

How it works in LeanLaw: A flat fee is set up on the matter at the outset. Depending on the firm's arrangement, the fee may be billed in full up front, upon completion, or in milestone-based installments. LeanLaw accommodates all of these structures.

What bookkeepers need to know:

-

Revenue recognition for flat fees is more nuanced than hourly billing. A flat fee paid upfront is generally held in trust until it is earned — the definition of "earned" varies by state bar rules and the specific fee agreement.

-

Some flat fees are considered earned upon receipt (non-refundable engagement fees in certain jurisdictions); others must be held in trust until the work is complete

-

This is one of the most common trust accounting errors in law firms — flat fee payments are deposited directly into the operating account rather than being held in trust first.

-

Always review the fee agreement and your state's bar rules before deciding how to handle flat fee deposits

-

LeanLaw allows you to set up flat fee matters and generate invoices at the appropriate milestone or completion point

ProAdvisor tip for bookkeepers: When onboarding a new flat fee matter, ask the attorney directly: "Is this fee earned upon receipt, or does it need to go into trust first?" Don't assume — the answer has direct implications for how you record the deposit.

Evergreen Retainer

What it is: An evergreen retainer is a trust account funding arrangement where the client maintains a minimum balance on deposit at all times. As the attorney bills against the retainer, the client is required to replenish it to the agreed minimum. It "stays green" — always funded.

How it works in LeanLaw: The firm sets a retainer threshold for the matter. As invoices are generated and trust funds are applied, LeanLaw tracks the remaining trust balance. When the balance falls below the threshold, a replenishment request is automatically triggered, prompting the client to send additional funds.

What bookkeepers need to know:

-

Evergreen retainers require careful trust account management — every deposit and disbursement must be tracked at the matter level

-

When a client replenishes their retainer, that deposit goes into trust (not income) and must be recorded as a trust liability in QuickBooks

-

When trust funds are applied to a paid invoice, the entry moves money from the trust account to the operating account and records the revenue

-

LeanLaw's trust ledger tracks all of this by client and matter, making reconciliation much more straightforward than manual methods

-

Watch for matters where the trust balance has dropped below the threshold but the client hasn't replenished — this creates a risk that the firm will advance costs or time without funds to cover them

Why attorneys love this model: It keeps cash flow predictable. The firm always has funds on hand to cover ongoing work, reducing the risk of carrying large accounts receivable balances.

Contingency Fee

What it is: The attorney receives no fee unless the case is won or settled. Upon a successful outcome, the attorney collects a percentage of the recovery — typically 33% to 40% in personal injury cases, though it varies by case type and jurisdiction.

How it works in LeanLaw: Contingency matters are tracked in LeanLaw like any other matter, but no invoices are generated during the life of the case. Expenses advanced on behalf of the client (filing fees, expert witnesses, medical records, etc.) are tracked against the matter and deducted from the settlement at the end.

What bookkeepers need to know:

-

There is typically no revenue to record during the life of a contingency matter — only expenses are being tracked.

-

Client cost advances are recorded as either trust disbursements (if paid from trust) or firm expenses to be reimbursed (if paid from the operating account).

-

When a settlement is reached, the attorney's fee and reimbursed expenses are calculated, and the net proceeds are disbursed to the client.

-

Settlement funds are often received into the trust account first, then disbursed — the attorney's fee is transferred to the operating account, expenses are reimbursed, and the client's net share is wired out.

-

This settlement disbursement process must be documented precisely; LeanLaw's trust ledger and disbursement tools support this workflow.

-

Revenue from contingency fees is recognized at the time of settlement, not before.

Common bookkeeping mistake: Failing to track expenses and reconcile advanced fees during a contingency matter, resulting in those costs being written off rather than reimbursed from the settlement.

Hybrid Billing

What it is: A combination of billing types on the same matter. For example, a client might pay a flat fee for the initial phase of a case and then transition to hourly billing if litigation becomes necessary. Or an attorney might charge a reduced hourly rate with a small contingency component built in.

How it works in LeanLaw: LeanLaw is flexible enough to accommodate hybrid arrangements. Matters can be structured with different billing types across phases, and the platform allows manual invoice adjustments to reflect custom arrangements.

What bookkeepers need to know:

-

Hybrid matters require clear documentation of which billing type applies to which phase or scope of work

-

Revenue recognition rules may differ across the phases — the flat fee portion and the hourly portion are treated differently

-

Communicate closely with the billing attorney to ensure invoices are being generated correctly for each phase

-

When in doubt, ask for a copy of the fee agreement — it's the source of truth for how the matter should be billed and recorded

Subscription / Recurring Legal Fees

What it is: An increasingly popular model — particularly for business clients — where the client pays a fixed monthly fee for ongoing legal services. Think of it as a legal services retainer billed on a recurring basis.

How it works in LeanLaw: Recurring invoices can be set up in LeanLaw to automatically generate on a set schedule, streamlining the billing process for subscription-based clients.

What bookkeepers need to know:

-

Monthly subscription fees are generally recognized as revenue in the month they're billed, consistent with standard accrual accounting

-

Unlike retainer deposits held in trust, subscription fees paid in advance may be recorded as deferred revenue until the service period is complete — confirm with the firm's CPA how they prefer to handle prepaid subscription arrangements

-

Track whether subscription clients are paying consistently; recurring billing makes it easy to spot lapsing payments early

A Quick Reference: Billing Types at a Glance

Billing Type |

Revenue Recognized When |

Trust Account Involved? |

Key Bookkeeper Watch-Out |

Hourly |

Invoice sent |

Often (retainer) |

Unbilled time entries |

Fixed Fee |

Earned per agreement |

Usually yes |

Premature income recording |

Evergreen Retainer |

Applied to the invoice |

Always |

Replenishment tracking |

Contingency |

Settlement reached |

Yes (settlement funds) |

Expense tracking during case |

Hybrid |

Varies by phase |

Depends on structure |

Phase-by-phase documentation |

Subscription |

Monthly billing period |

Rarely |

Deferred revenue treatment |

The Golden Rule for Every Billing Type

Regardless of which billing arrangement a matter uses, one principle applies universally in legal bookkeeping: unearned client funds belong in trust, not in the operating account. The moment you move money from trust to operating before it's earned, you've created a compliance problem — even if it was an honest mistake.

LeanLaw is designed to help you get this right. Its trust accounting workflows, matter-level ledgers, and QuickBooks integration create a clear paper trail for every dollar that flows through the firm. But the software can only do its job if the person managing it understands the rules behind each billing type.

When you know how each billing arrangement works — and how LeanLaw handles it — you stop being a bookkeeper who just records transactions and start being a trusted financial partner to the firm. That knowledge is what separates a good legal bookkeeper from a great one. Now you have it.

Questions about how a specific billing arrangement should be handled in LeanLaw? Leave a comment below or connect with us — we love helping bookkeepers navigate the nuances of legal accounting.

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.